North Carolina needs smart property tax relief, not reckless revenue limits

Property taxes are the backbone of local public services in North Carolina, funding everything from school buildings and libraries to fire departments and parks. But when property values rise rapidly in a housing market already short on affordable options, higher tax bills can strain incomes and displace long-time residents. That reality has prompted renewed legislative attention to property tax reform. The challenge now is ensuring those efforts provide meaningful relief without jeopardizing the public services communities depend on.

House Speaker Destin Hall has convened a bipartisan House Select Committee on Property Tax Reduction and Reform, and Senate President Phil Berger announced that he’s convening a group of Republican senators to “examine and recommend property tax reforms.” We’ve written before about good options for property tax relief, which would support the people who need it most without jeopardizing the local services we all rely on.

But some lawmakers are revisiting old and tired playbooks to put severe and failed restrictions on property taxes; strict property tax limits create more problems than they solve, and they would leave NC’s towns and counties worse off.

NC’s current property tax system can drive housing affordability issues and inequities

Property taxes are a factor of both tax rates and a home’s assessed value, and when home values rise more quickly than people’s wages, higher taxes can strain people’s ability to afford housing and basic needs and exacerbate displacement pressures. This is especially true for long-time homeowners with low incomes — such as seniors on fixed incomes — who see a sudden jump in their property taxes after an assessment. It’s important to remember that property taxes affect affordability for renters as well, who pay them indirectly through rent payments.

Major increases are more likely when appraisals don’t happen often. In North Carolina, counties must conduct appraisals at least every eight years, but many counties have moved to a four-year cycle so that changes are more manageable for residents. Wake County, which has seen some of the biggest increases in home values, will soon shorten the revaluation cycle to every two years.

Without effective policies, property taxation can contribute to economic and racial inequities

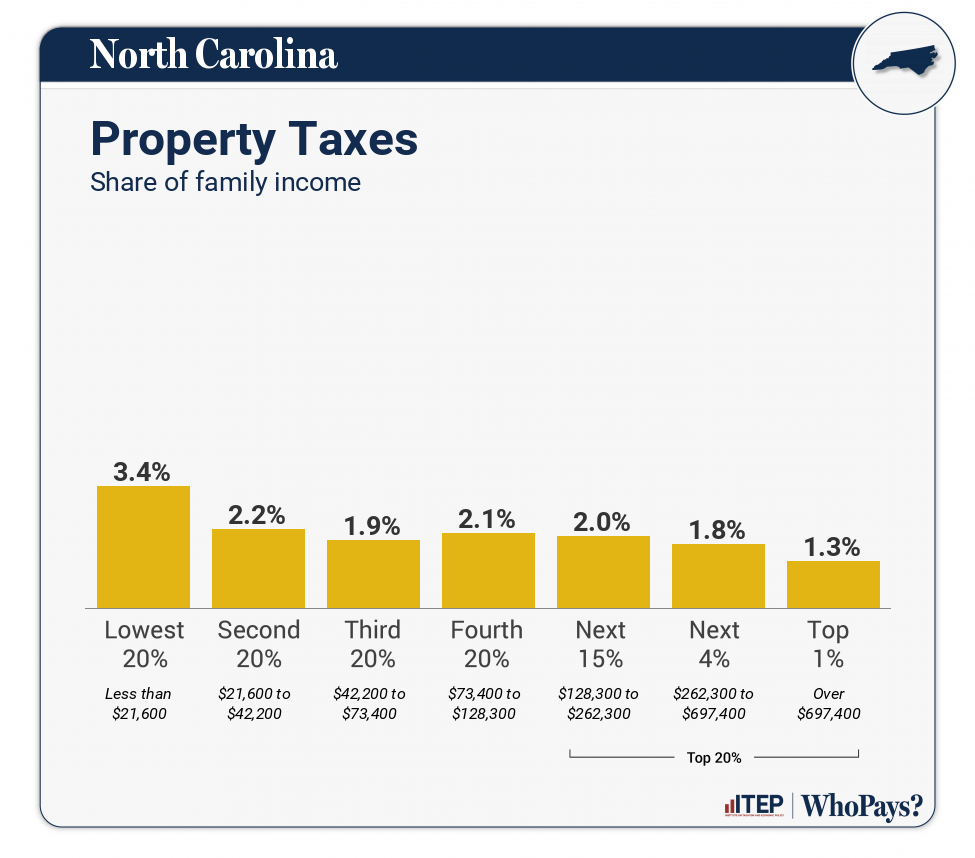

Property taxes in NC are regressive, meaning that households with higher incomes pay a smaller portion of their income in these taxes, while households with lower incomes pay a larger share. Property tax disparities also make our tax system more racially inequitable. Research has found that homeowners of color, and especially Black homeowners, are more likely than white homeowners to have their homes be overvalued for tax assessment and that they are less likely to successfully appeal high assessments. Advocates from the NC Housing Coalition have been working with residents in Wake and Orange counties so they can push back against inequitable appraisals.

The three existing property tax relief programs in NC are very narrowly tailored and have onerous applications. To qualify, homeowners must be over 65 or have a permanent disability and a very low income or be disabled veterans.

Property taxes are the most important source of revenue for local governments

Any changes to property taxes need to take into consideration that they are the biggest source of revenue for local governments. One-third of NC’s county and municipal revenues came from property taxes in 2024.[1] (The next-largest source was intergovernmental transfers at 14 percent. These are primarily funds from state and federal sources, not revenues generated from local sources.)

Property taxes are especially important because they provide a relatively stable form of revenue — property tends to hold its value over time. And in NC, local governments have limited options when it comes to funding their services. Unlike in some states, cities and counties can’t create local income taxes, and they’re also limited in their ability to raise sales taxes.

Local governments are already under pressure from federal and state cuts

Local governments are already under pressure because of state tax cuts and federal cuts to key programs like SNAP food assistance and Medicaid that will put more strain on local services. Further restraining their ability to raise public funds will harm local services without addressing housing affordability.

Property tax limits shift burdens and hamstring local governments

Decades of research on strict property tax limits, many of which were adopted during the anti-government “tax revolts” of the 1970s, show negative consequences on local revenues, services, and housing markets. These policies can take a few forms, whether limiting tax rates, assessed property values, total revenue, or some combination of these.

Most recently the House Select Committee on Property Tax Reduction and Reform heard from the right-wing Tax Foundation with a proposal for a “levy limit” which would cap overall revenue growth from property taxes, excluding new construction. The property tax

levy refers to the total amount of revenue a town or county brings in from property taxes. This means that if rising property values would lead the total levy to grow above the limit, property tax rates would automatically decrease to keep the levy under the cap. The example proposed by the Tax Foundation wouldn’t allow the levy to grow any faster than inflation.

Levy limits effectively tie future local budgets to current spending, without consideration for how service needs, or the cost of providing those services, might change in the future. They take the ability to raise revenue out of future elected leaders’ hands without knowledge of whether levels of funding from other sources like state aid will remain reliable. While these policies usually allow voters to override the limits at the ballot box, these elections are often held during off years, and may have low turnout. Ballot initiatives related to tax limits in Colorado have been decided by fewer than one-third of eligible voters.

Tax caps make local governments more reliant on state funding and regressive fees

Research on restrictive property tax limits in other states highlights a wide range of unintended consequences. The most consistent finding is that after state limits are enacted, local governments shift their budgets to rely more on other forms of revenue, specifically state aid and user fees. State aid doesn’t offer the stability that property taxes do and generally decreases during recessions. In NC, where legislators have committed to over a decade of income tax cuts for the wealthy few and profitable corporations, the state budget is facing its own revenue crisis.

- Massachusetts’ Proposition 2 ½ limits a municipality’s property tax levy growth to 2.5 percent each year, excluding new construction. Annual revenues from property tax also can’t be higher than 2.5 percent of the total value of property.

- After Prop 2 ½ went into effect in 1980, local governments began to rely more heavily on state aid, but its availability shifted with economic cycles and state policy decisions. When state aid receded, wealthier communities often voted to raise their local property taxes, leaving lower income cities and towns with few options other than to cut services.

If local governments can’t get support from the state, their other options are to make up revenue loss from property tax limits with user charges, fines, and fees. But revenue from user charges is generally tied to specific services such as water or trash collection and can’t be broadly used for public services. Raising fines and fees will also make the tax system even more regressive, with the impacts falling hardest on people with the lowest incomes.

If there aren’t alternatives, local governments cut services

When local governments can’t rely on the state to backfill budget gaps, property tax caps are likely to lead to public service cuts. In states where property tax limits were put into place recently, local governments are slashing the services that residents rely on. These cuts include closing community pools, considering deep cuts to emergency services, reducing service hours and staffing at libraries, and more.

- New York State’s Property Tax Cap imposes an annual levy cap of no more than 2 percent and has been in place since 2011. Even as the economy improved after the Great Recession, county level spending in the state decreased significantly in the years after the cap was imposed, including declines in education spending and steep declines in health and community services. A study also found that public schools in New York that rely on property taxes more heavily to fund their budget experience fiscal constraints and tend to cut expenses related to non-teaching staff, administration, and school buses.

Limiting property assessments distorts the housing market

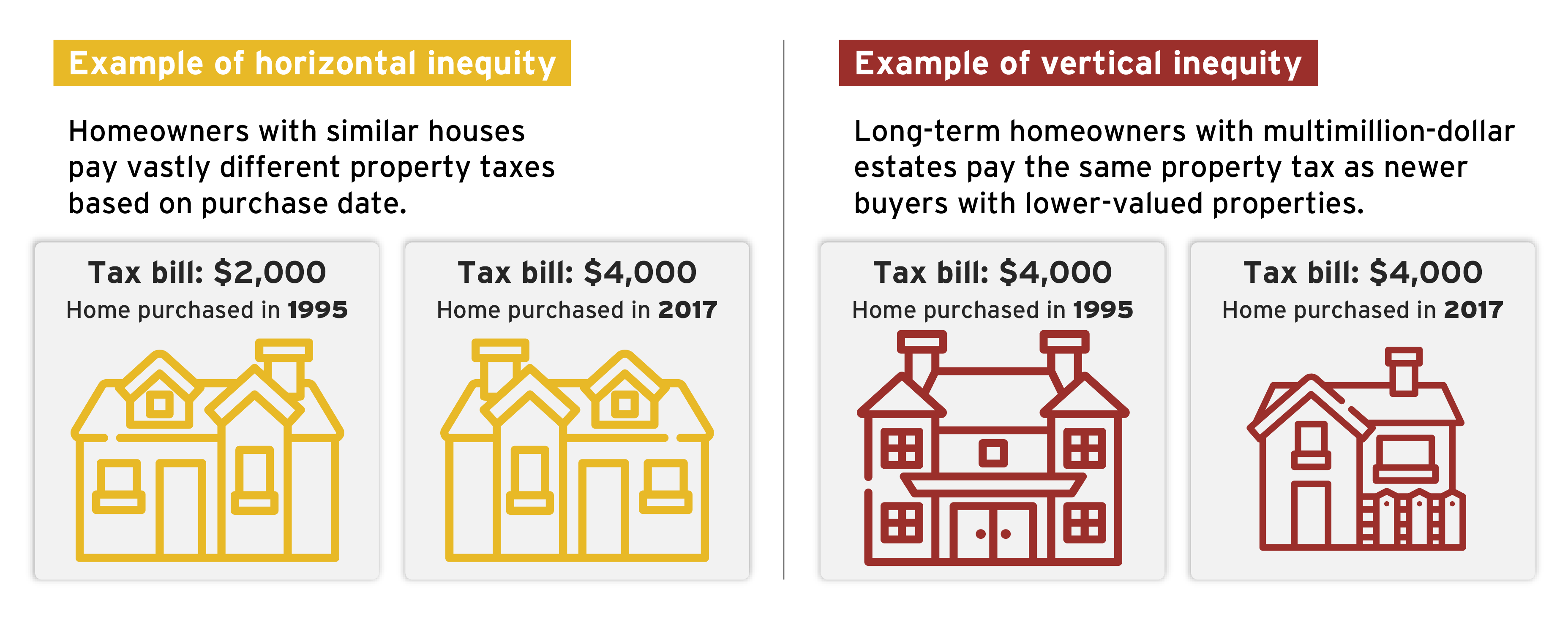

Limits on property assessments present another host of problems. Because assessments generally reset when a home is sold, these restrictions create massive and irrational differences in tax payments between long-term and newer residents.

- California’s Proposition 13, passed in 1978, limits municipal tax rates to 1 percent of total assessed value and limits the annual growth of assessed value to no more than 2 percent. Assessed values reset to the actual market rate when a home is sold.

- After Prop 13’s passage, California counties came to rely heavily on state funds, and the state spent significant reserve funds supporting county services and schools. The consequences for the housing market were new inequities based purely on when someone purchased their home. This means two neighboring and otherwise identical homes could have vastly different property tax payments because one was purchased 20 years earlier and was subject to assessment limits over that time.

Property tax limits can deepen racial inequities and disparities between wealthy and low-income municipalities

Property tax limits don’t address the racial inequities that already exist in the tax system. Rather research shows they widen racial inequities, with white homeowners seeing the largest reductions in their effective tax rate. In California, Prop 13’s restrictions have disproportionately benefited white homeowners who tend to have owned their homes for longer. On average, white homeowners get annual property tax breaks that are more than 80 percent higher than Black homeowners and more than twice as high as Latine homeowners.

Levy limits often exclude new construction. This means that high-growth areas are able to grow their revenue from taxes on new properties. (Although because new construction and new residents also need services, it doesn’t necessarily mean they can keep up with service needs.) Relying on new construction to increase local revenues can deepen inequities between fast-growing urban centers and rural areas. Relying on voter overrides to allow revenue increases can also widen the gap. In Massachusetts, wealthy towns have been far more likely to approve increases than lower income communities, worsening the gaps in their fiscal stability.

Better state policy can offer an actual solution

Fundamentally, arbitrary tax caps imposed by states limit a local government’s ability to raise funds to reflect the actual needs of their constituents. But NC has better policy options. As an incremental step, the state could expand existing relief programs so they reach more people, for example by raising income limits or lowering the age limit. The legislature could allocate state funds to reimburse local governments for additional costs, instead of committing to state tax cuts. Lawmakers who are serious about improving property tax policy could also pursue a truly comprehensive and equitable policy solution: a statewide “circuit-breaker” program that’s administered through state tax filing and provides affordability in property taxes to both homeowners and renters.

Property tax limits may sound simple, but they risk making housing less stable and local services weaker. If lawmakers are serious about affordability, they should choose targeted relief — not blunt caps that shift costs and deepen inequities.

[1] Based on Annual Financial Information Reports submitted to the NC State Treasurer

{kind=link}

{kind=link}